In this study, we examine how different household configurations are affected by the current system. Our focus lies on analyzing the perverse incentives and on providing specific reform recommendations for the existing system. We also discuss the key findings in the following podcast:

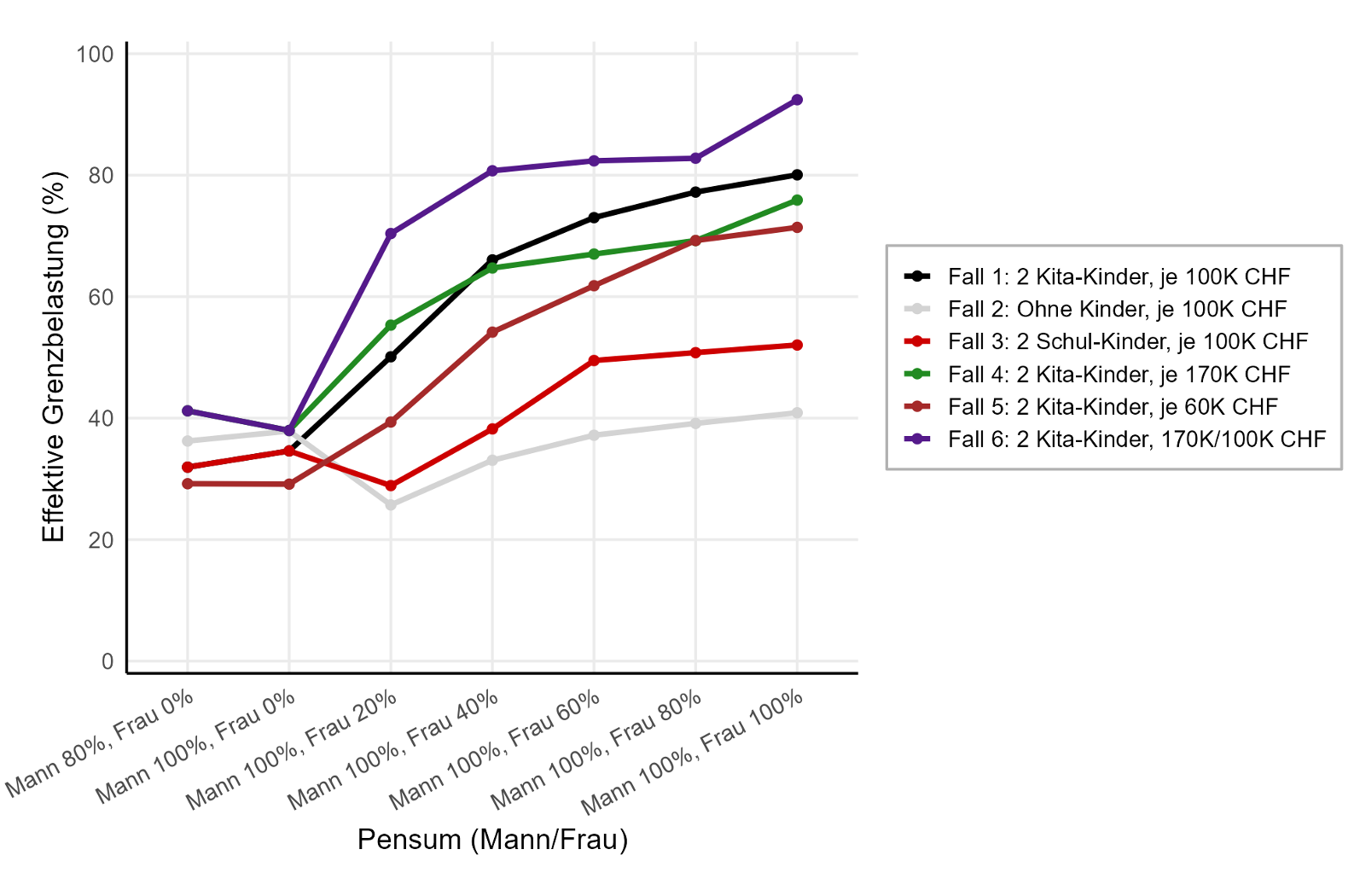

Specifically, we examine the following constellations:

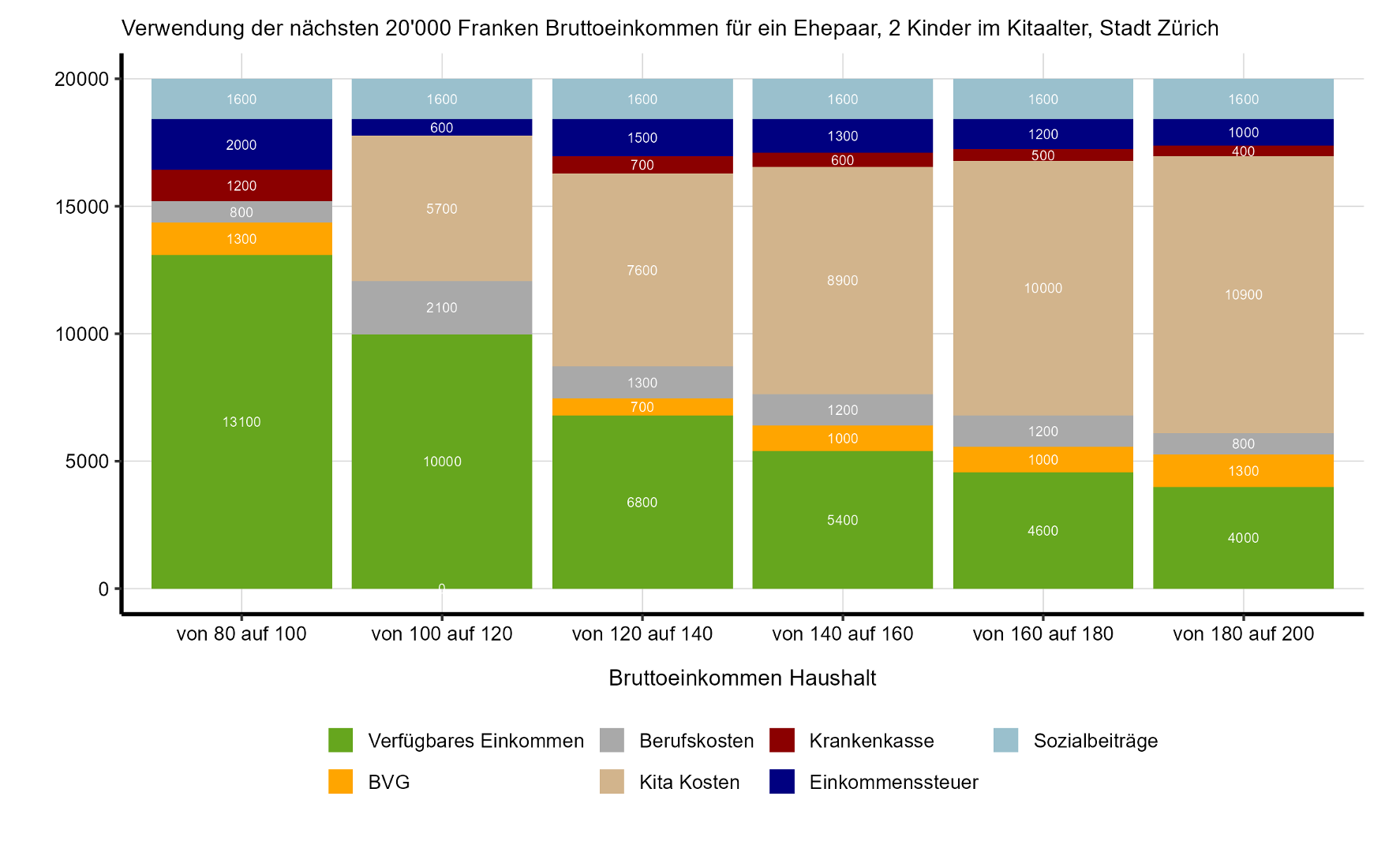

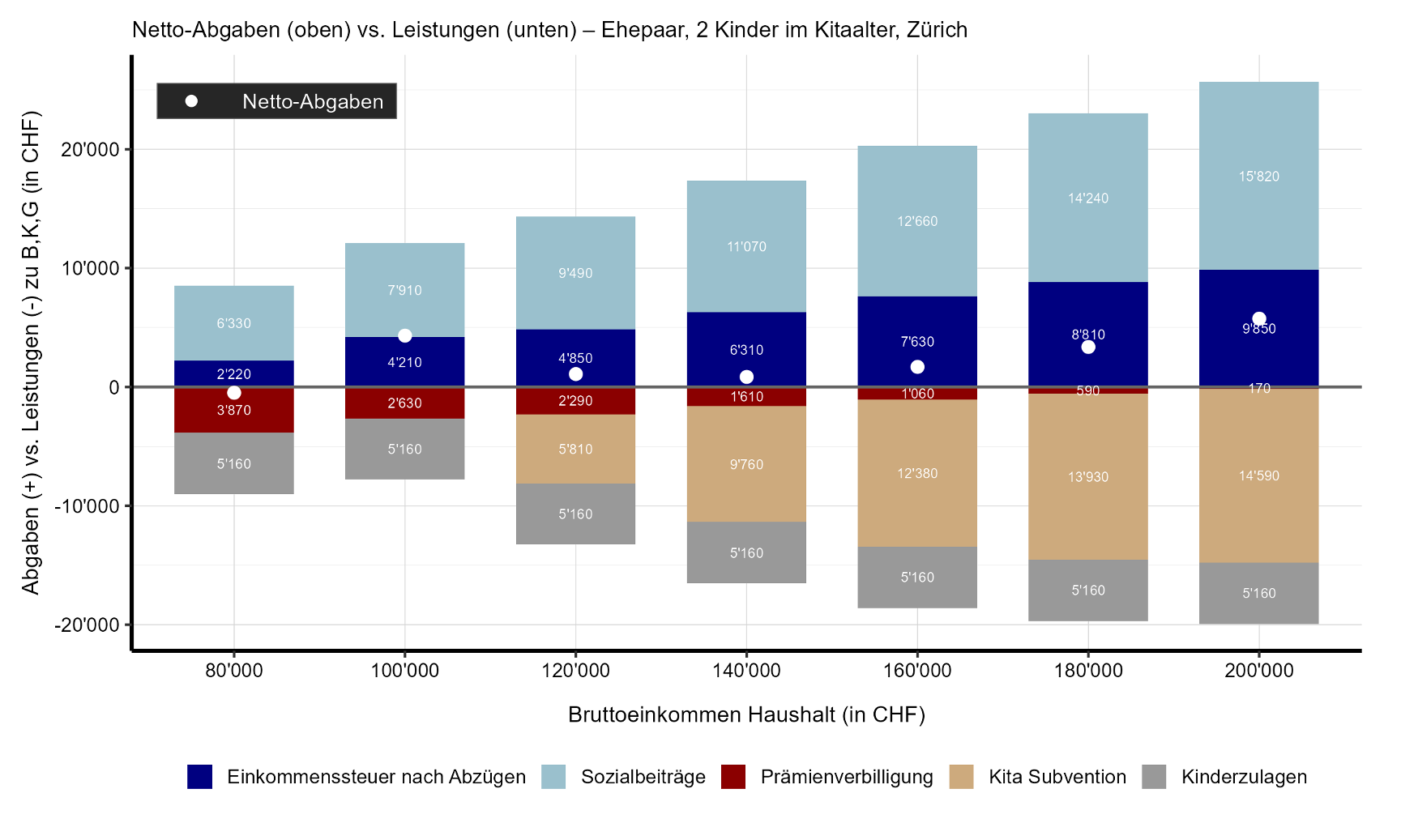

Both spouses could earn a gross income of CHF 100'000 working full-time. They have two children of preschool age (basic scenario).

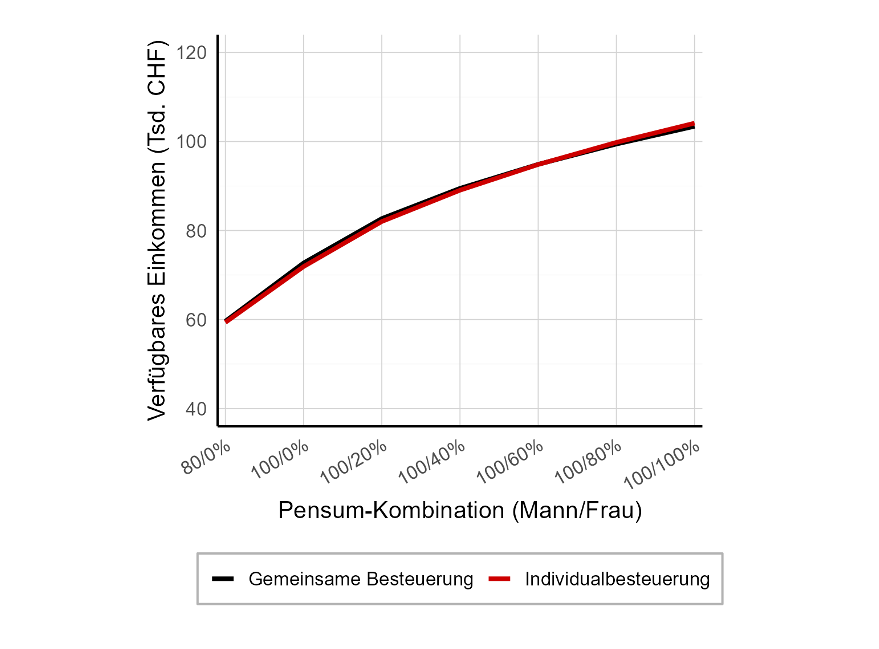

Both spouses could earn a gross income of CHF 100'000 working full-time. They don't have children.

Both spouses could earn a gross income of CHF 100'000 working full-time. They have two children who go to school.

Both spouses could earn a gross income of CHF 170'000 working full-time. They have two children of preschool age.

Both spouses could earn a gross income of CHF 60'000 working full-time. They have two children of preschool age.

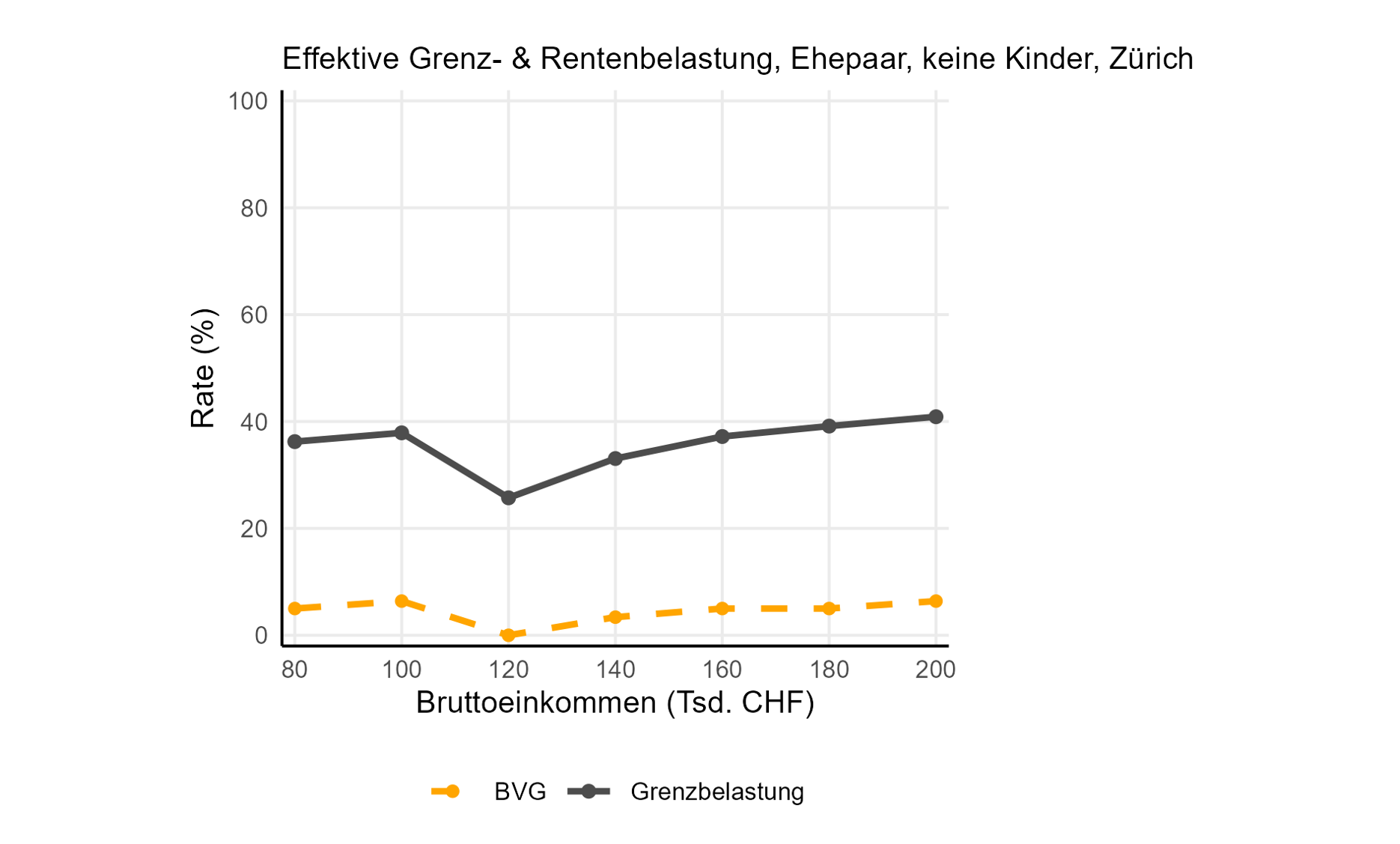

The couple could earn a gross income of CHF 170'000 (husband) and CHF 100'000 (wife) working full-time. They have two children of kindergarten age.

The main conclusions are as follows:

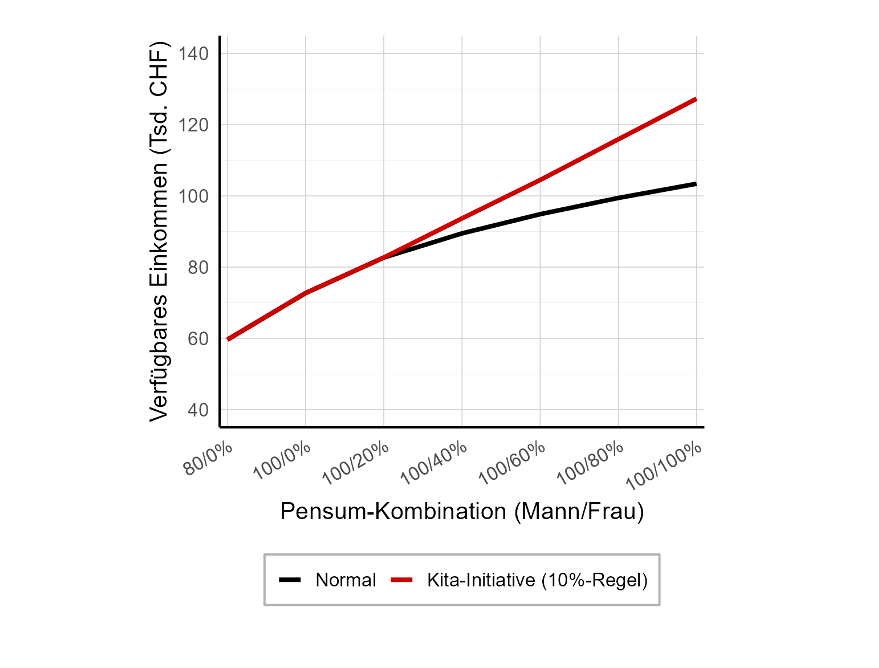

We can identify two main thrusts in the reforms:

How to achieve this:

Full Professor of Tax Law / Director

Head of Tax & Trade Policy / Director